Every year the FAA releases its Civil Airmen Statistics, and every year the aviation media runs the same headline: pilot shortage, pipeline growing, record numbers. And they're right — sort of. The numbers do show record production. But a closer look at the 2025 data reveals something that nobody in mainstream aviation media is talking about, and it has serious implications for anyone planning a career at the airlines.

I've spent time digging into these numbers — not just the headline figures, but the certification-by-certification breakdown. What I found is a story about a pipeline that's producing more than it can ever place, and a category of certificate that quietly tells the whole story.

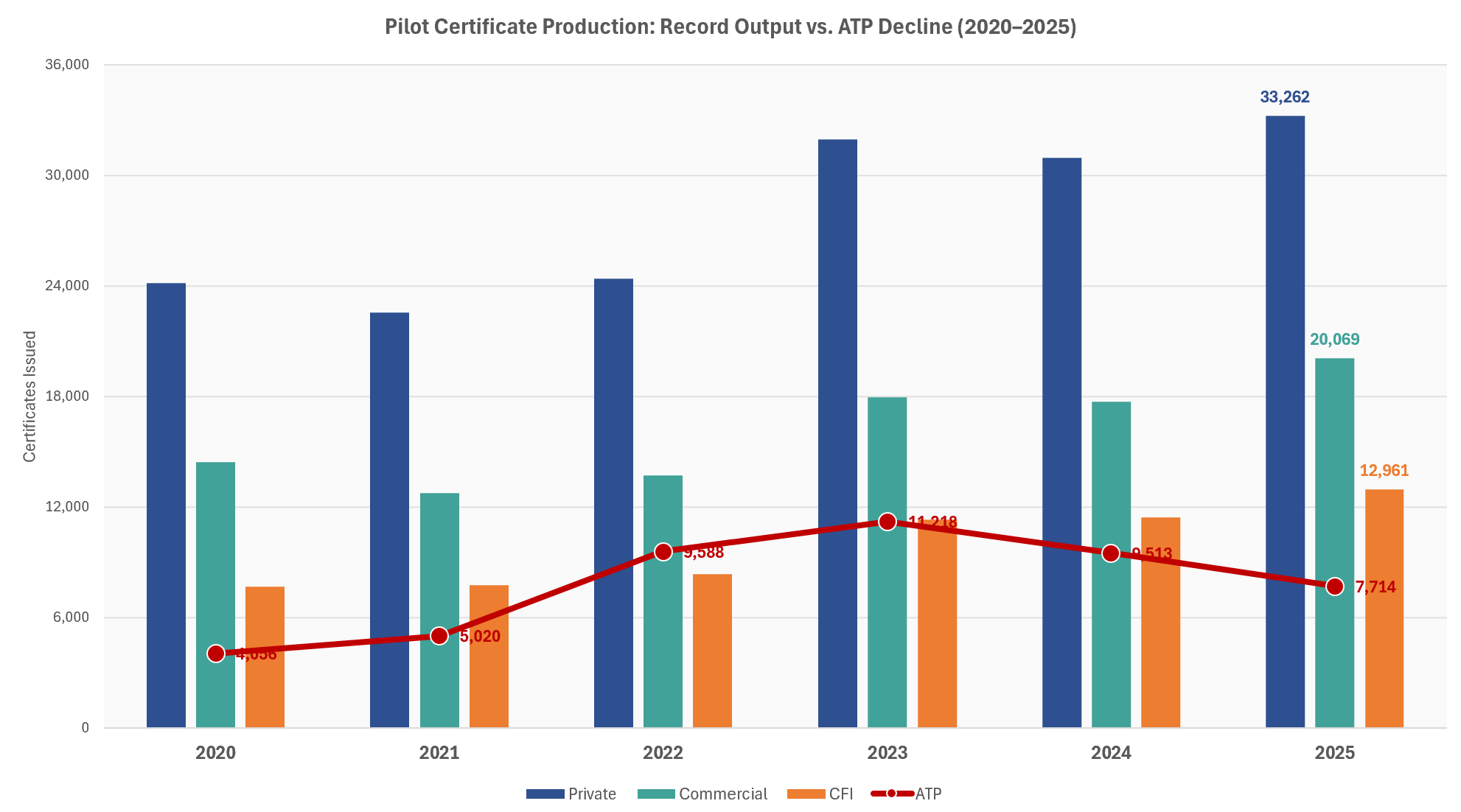

What the 2025 numbers actually show

Here's the chart I put together from the FAA's 2025 airman statistics data. Take a moment with it, because it's doing a lot of work.

Source: FAA Civil Airmen Statistics 2020–2025. Private (blue), Commercial (teal), CFI (orange), ATP initial issuances (red line).

Private pilot certificates: record high at 33,262. Commercial certificates: record high at 20,069. CFI issuances: record high at 12,961. And ATP initial issuances — the one certificate that actually gets you onto a jet — down for the third straight year, from 11,218 in 2023 to just 7,714 in 2025. A 31% drop in three years while everything else is surging.

The pipeline nobody's talking about

When people say "pilot shortage," they usually mean a shortage of airline pilots. That's the job most career-track pilots are building toward. And the assumption is that if you're producing more private and commercial pilots, the airline supply chain is improving. That assumption has a flaw.

Getting from a commercial certificate to an airline seat is a long, structured process. You need 1,500 hours for an ATP certificate (or 1,000/1,200 via a four-year aviation degree or other accredited program, 750 via the military). That takes years of instructing, charter flying, or corporate work. Then you need to actually get hired — and there's a hard ceiling on how fast airlines can grow.

In just the last three years, the U.S. has produced approximately 55,000 commercial pilot certificates. Airlines will hire roughly 5,000 pilots per year over the next decade. That's an 11-year queue just from the last three years of production alone — and production is accelerating.

Airlines are constrained by factors that have nothing to do with pilot supply: aircraft orders and delivery timelines (Boeing and Airbus are both running multi-year backlogs), gate availability, infrastructure capacity at major airports, and passenger demand growth, which historically averages around 2% per year. Carriers simply don't grow faster than that in any sustained way, and their hiring follows accordingly.

The other known factor is retirements. At the mandatory retirement age of 65, the airlines know years in advance how many captain slots will open up. That math is stable and predictable. Combined with modest fleet growth, the result is a fairly consistent hiring rate of around 5,000 pilots per year across the U.S. majors, regionals, and cargo carriers — through approximately 2035.

The pipeline flow diagram

Here's the visual I built to explain this. Each stage represents a real gate in the certification process, and the constraints on the right side of the funnel show why the math doesn't add up for everyone in the pool.

Run the numbers yourself

The queue calculator below lets you adjust the assumptions. The defaults are conservative — 18,000 new commercial certs per year (slightly below 2025's record pace) and 5,000 airline hires per year. Drag the sliders and watch the queue grow. Try pushing the hiring rate up to what it would take to actually clear the backlog.

So what does this mean for you?

If you're a student pilot or a newly certificated commercial pilot aiming for the airlines, this data isn't meant to discourage you. It is meant to calibrate your expectations — and more importantly, your strategy.

The timeline is longer than the marketing suggests. Flight schools and aviation universities have every incentive to emphasize the shortage narrative. The reality is that the shortage is concentrated at the captain level at major carriers, driven by retirements. The first-officer pipeline is actually well-stocked, and competition for regional first-officer slots is increasing, not decreasing.

The ATP decline is the canary in the mine. When ATP initial issuances drop three years in a row while commercial production is surging, it means one of two things: pilots are taking longer to reach ATP minimums, or a growing number are leaving the pipeline before they get there. Both scenarios point to a pipeline that's wider at the top than it's ever been, and just as narrow at the bottom.

Non-airline aviation careers are real and growing. Corporate aviation, charter, agricultural, air medical — these sectors are also hiring, also growing, and in many cases offer quality-of-life advantages that are genuinely competitive with the regionals. Don't measure success only by the airline yardstick.

I'll be covering this in more depth in the podcast and in a short-form series on YouTube. If you have questions or you're looking to talk through your specific training path, reach out — this is exactly the kind of planning conversation I have with students regularly.

Want to verify the numbers yourself? I'm sharing the source data and my projection spreadsheet because this is an important conversation and you should be able to check my work.

Want to dig deeper?

Subscribe to the Checkride Insights podcast for the full breakdown — and follow along on YouTube for the short-form version of this data.